Market volatility can feel deeply unsettling. When the S&P/ASX 200 dropped over 37% in weeks during March 2020, or when inflation shocks in 2022 triggered sharp sell-offs, even seasoned investors questioned their strategy. More recently, AI-driven rallies pushed the Nasdaq up 40% in 2024 before pullbacks of 10-15% in early 2025 reminded everyone that rapid gains can reverse just as quickly.

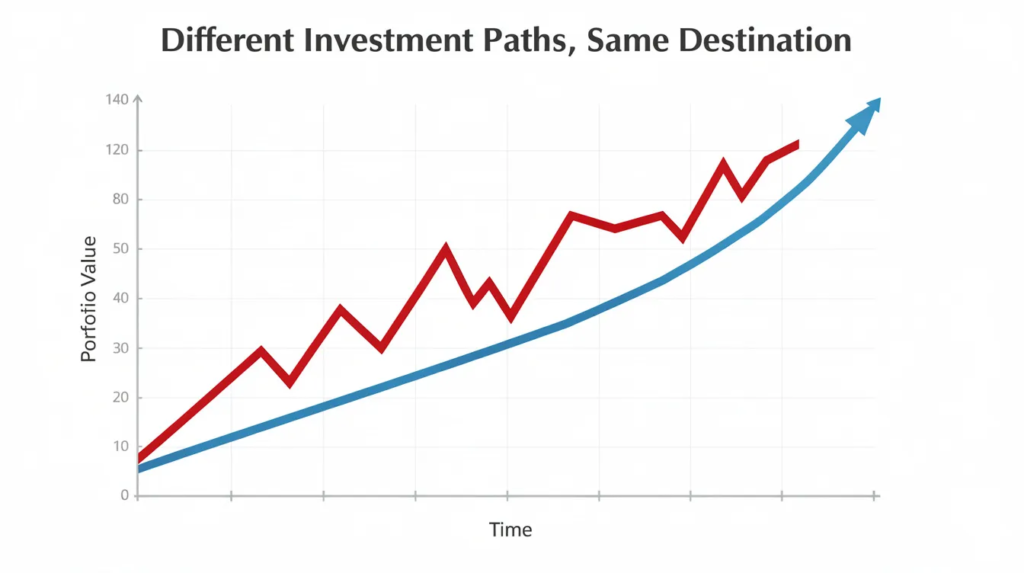

Even a well-constructed diversified portfolio can swing 20-30% during severe market turmoil. Yet history consistently shows that investors who stay invested through volatile periods generally outperform those who attempt to jump in and out. For Australian readers, this means accepting that superannuation balances and investment portfolios will naturally rise and fall. This is a feature of long-term investing, not a flaw. This sits within a broader framework — you can explore how investment strategies are applied in practice.

This article focuses on practical, actionable ways to stay invested during volatility. You’ll find concrete examples, data-driven guidance, and strategies tailored to Australian investors navigating current market conditions. Money Path serves as an Australian investment and advice partner, helping clients build, monitor, and maintain long-term strategies through changing market conditions.

What Is Market Volatility and How Does It Show Up in Your Portfolio?

Volatility refers to the speed and size of price movements in assets like shares, bonds, property, and currencies. In simple terms, it measures how much and how quickly the market value of your investments can change. These movements are a normal part of how market cycles, including bull and bear phases, unfold over time.

During March 2020, the ASX 200 experienced daily drops exceeding 5-10%. Yet despite this dramatic bear market, the index ended 2020 in positive territory. This illustrates a crucial point: intra-year swings of 30-40% can occur even when annual returns finish positive.

Volatility cuts both ways. Rapid gains during the 2024 AI rally pushed tech-heavy portfolios up 20-30% in months, tempting many investors to lock in profit through premature selling. The emotional toll of upside volatility can be just as challenging as downturns.

Different asset classes carry different typical volatility levels:

Asset Class | Typical Annual Volatility |

|---|---|

Cash | 0-2% |

Bonds | 4-8% |

Diversified equities | 12-18% |

Single stocks | 25-40% |

Crypto | 50-100% |

A typical Australian super fund with 50% Australian shares, 30% international, 15% bonds, and 5% cash experiences roughly 10-15% annual volatility versus 25% for a pure equity market exposure.

Why Markets Become Volatile: Causes, Not Excuses

Market volatility arises from rapid price adjustments to new information. When macroeconomic data shifts, earnings surprise, or geopolitical tensions flare, millions of investors and algorithms react simultaneously, often overshooting in both directions before finding equilibrium.

Consider the RBA’s eleven interest rate hikes between 2022-2023. Australian bank and property stocks dropped 20-30% as interest rates rose faster than expected, crushing property trusts by 25%. When interest rates rise, bond prices typically fall, and equities face headwinds from higher borrowing costs.

US inflation surprises in 2022, when CPI hit 9%, triggered global equity sell-offs of 20% or more. Meanwhile, the AI optimism of 2023-2025 saw Nvidia surge 200% before valuations prompted corrections. These episodes demonstrate that while specific causes differ, volatility itself is a recurring, normal feature across decades of stock market history.

Trying to predict each bout of volatility is extremely difficult. The primary basis for building resilient portfolios is assuming volatility will happen, not attempting to avoid it through perfect timing.

The Cost of Trying to Time the Market

Market timing—selling when markets fall and planning to buy back lower—seems logical during scary headlines. The problem is that the best and worst days cluster together, often within days of each other around market turning points.

Consider this scenario: $100,000 invested in a broad share index from 2000 to 2025 would grow to approximately $400,000 when fully invested, delivering around 7% annually. Missing just the 10 best days drops that to roughly $200,000. Missing the 20 best days leaves you with around $100,000, barely keeping pace with inflation. These patterns are commonly seen when examining why many investors underperform the market over time.

The emotional cycle compounds this problem. Investors typically move from optimism to anxiety to fear, eventually capitulating into cash at precisely the wrong time. An Australian investor who moved to cash after the March 2020 fall and only reinvested in late 2021 missed a 50%+ rebound, locking in significant losses and underperformance.

Past performance demonstrates that timing attempts rarely succeed. The focus should be on time in the market, not timing the market.

Core Principles to Help You Stay Invested During Volatility

These principles work together as an integrated investment strategy. Focusing on time horizon, diversification, regular investing, and clear rules reduces the urge to react to headlines. Each principle reinforces the others, helping you navigate whatever market trends emerge. This also ties into broader decisions around how asset allocation evolves across different life stages.

1. Anchor on Your Long-Term Goals and Time Horizon

A 5-30 year financial goal—retirement, children’s education, or business proceeds—far outweighs the significance of a single volatile month. Since the early 1990s, the Australian share market has delivered positive returns in roughly 75% of calendar years, with positive years averaging gains around 15% versus losses around 10% in negative years.

A 35-year-old investing for retirement at 67 will experience many corrections and several bear markets. Yet they need growth to combat inflation and build retirement savings that support their lifestyle. Write down 2-3 specific long-term financial goals and refer back to them when tempted to change strategy during turbulence.

2. Build Diversification Before the Storm, Not During It

Diversification means spreading investments across asset classes—Australian shares, global shares, bonds, listed property, and cash—and within them across sectors and geographies. The goal is reducing credit risk and overall portfolio volatility.

During the 2022 tech sell-off, concentrated technology portfolios dropped 35% or more, while a diversified 60/40 portfolio fell only 15-20%. Fixed income and defensive holdings provided ballast when equities struggled. Historical data from the US aggregate bond index and aggregate bond index performance shows bonds often hold value during equity market stress, though not always.

Diversification isn’t about owning many things. It’s about owning assets that don’t move the same way for the same reasons—achieving low correlation between your holdings.

3. Use Regular Investing to Smooth Out the Ride

Dollar cost averaging involves investing a fixed amount at regular intervals regardless of market levels. This approach means buying more units when prices are low and fewer when prices are high, reducing the impact of poor timing. This approach is often used when deciding whether to invest a lump sum or phase investments over time.

Consider investing $1,000 monthly into a diversified fund throughout 2020-2023. Despite the crash and recovery, this regular investing approach often outperformed lump-sum timing attempts by 7% or more, as contributions captured lower prices during the downturn.

Align regular contributions with salary dates and superannuation contributions to make the strategy automatic. This removes emotion from investment decisions and transforms market stress into an investment opportunity.

4. Keep Enough Cash So You’re Not Forced to Sell

An emergency cash buffer—typically 3-6 months of essential expenses—prevents forced selling during downturns. This money covers near-term needs like rent, mortgage payments, and tax bills, ensuring your portfolio stays intact through volatile periods.

An investor who loses their job during a downturn but maintains adequate cash reserves can leave their portfolio alone to recover. Without this buffer, they might sell at exactly the wrong time, crystallising significant losses. The right cash level depends on your financial situation, job security, and upcoming known expenses.

5. Set Clear Rules for When You Will Review and When You Won’t React

Schedule portfolio reviews quarterly or twice yearly rather than checking balances daily. Create simple rules: only make changes when personal circumstances change, or when asset allocation drifts beyond 5-10% from targets.

Rebalancing—trimming assets that have grown strongly and adding to those that have lagged—feels counter-intuitive during volatility but adds 0.5-1% annually over time. After strong US tech performance in 2023-2025, rebalancing might mean shifting from outperforming growth stocks into underperforming defensive assets.

Document these rules with your financial adviser to maintain discipline through market stress.

6. Manage Your Emotions, Not Just Your Portfolio

Common triggers during volatility include fear from headlines, social media noise, and watching others move to cash. Simple behavioural tools help: take a 24-hour pause before acting, limit balance checks to monthly, and frame losses as temporary fluctuations rather than permanent.

A written investment policy acts as a guardrail when anxiety spikes. It reminds you that your particular needs and risk tolerance haven’t changed just because markets moved. Seeking guidance from a financial advisor isn’t weakness—it’s a way to outsource emotional burden and gain perspective. Many of these behaviours are reflected in common investment mistakes investors make over time.

Practical Steps to Take During a Volatile Period

When markets drop 15-20% over several weeks, the first step is doing nothing immediately. Research shows 90% of sharp moves recover within 6-12 months. Assess whether your financial goals have actually changed.

Review your allocation for drift from targets. Check whether any holdings’ fundamentals have genuinely deteriorated versus simply falling with broader markets. Consider tax-loss harvesting opportunities where appropriate.

Distinguish between reacting to market noise and responding to genuine changes in your own circumstances—like redundancy or illness. The former rarely helps; the latter requires thoughtful response. A stress-test showing a 20% drop delays retirement by 6 months, while reactive timing can lock in 2+ years of setback.

How Money Path Can Help You Stay Invested Through Volatility

Money Path serves as a partner for Australian investors seeking structured, evidence-based guidance through volatile markets. Rather than reacting to every headline, Money Path helps clients build clarity around their investment journey.

Working with Money Path involves clarifying goals, agreeing on appropriate risk levels, building a diversified portfolio, and establishing a written investment plan. This plan becomes your anchor when markets swing dramatically, ensuring decisions align with long term perspective rather than short-term fear.

Money Path provides ongoing monitoring and regular check-ins, helping distinguish between noise and meaningful changes. Scenario modelling shows clients exactly how a 20% market fall might affect retirement timelines, while guided rebalancing keeps portfolios aligned with targets.

For someone nearing retirement and worried about recent volatility, Money Path implements gradual de-risking and cash buckets covering 3-5 years of spending. For a business owner with lump-sum proceeds, Money Path designs a dollar cost averaging approach into diversified holdings, stress-tested against realistic scenarios. The focus remains on long term returns and education, never market timing or speculation.

Frequently Asked Questions About Staying Invested During Volatility

Should I move everything to cash when markets fall? Moving to cash carries substantial opportunity cost. Investors who shifted to cash after the 2020 fall and missed the subsequent rebound underperformed diversified investors by 30% or more. Cash yields typically 1-4% versus 8% for equities over the long term. Future performance may differ, but history suggests timing attempts fail more often than they succeed.

Is now a bad time to start investing if markets are volatile? There’s rarely a perfect “safe” entry point. Regular investing through volatility actually benefits from lower average costs. Historical data shows investing when the VIX exceeds 30 has delivered premium returns of around 2% annually. Your time horizon matters more than entry timing.

How much should I change my portfolio when I feel nervous? Minimal changes typically serve best. Revisit your risk tolerance, but avoid wholesale shifts driven purely by fear. Fear-driven changes cost approximately 2% annually in foregone returns. Focus on whether your circumstances have changed, not whether markets have moved.

What if I’m close to retirement—can I still stay invested? Yes. Strategies like gradual de-risking, cash buckets covering 2-5 years of spending, and maintaining growth assets for later years help manage sequence risk while preserving long term financial goals.

How often should I check my investments during volatility? Monthly or quarterly reviews work well. Frequent checking amplifies anxiety without improving outcomes. Studies show less frequent monitoring reduces emotional trading and improves adherence to strategy. Always read the financial services guide for any financial product before investing.

Bringing It All Together: Your Next Steps

Volatility is normal—it recurs several times per decade. Timing the market is costly; missing just 10 best days can halve your long term returns. Staying invested with a diversified, goal-aligned portfolio has historically rewarded patient investors across the great depression, global financial crisis, and countless other volatile periods.

This week, take two concrete actions: articulate or update your long-term goals, and review whether your current portfolio matches your risk tolerance and time horizon. Neither future results nor reliable indicator guarantees exist, but controlling your approach significantly improves your odds of success.

Book a conversation with Money Path to stress-test your current strategy against realistic volatility scenarios. While no one controls markets, you can control your response—and Money Path exists to help you do exactly that.